Market Roadmap / Insights (04/30/2026)

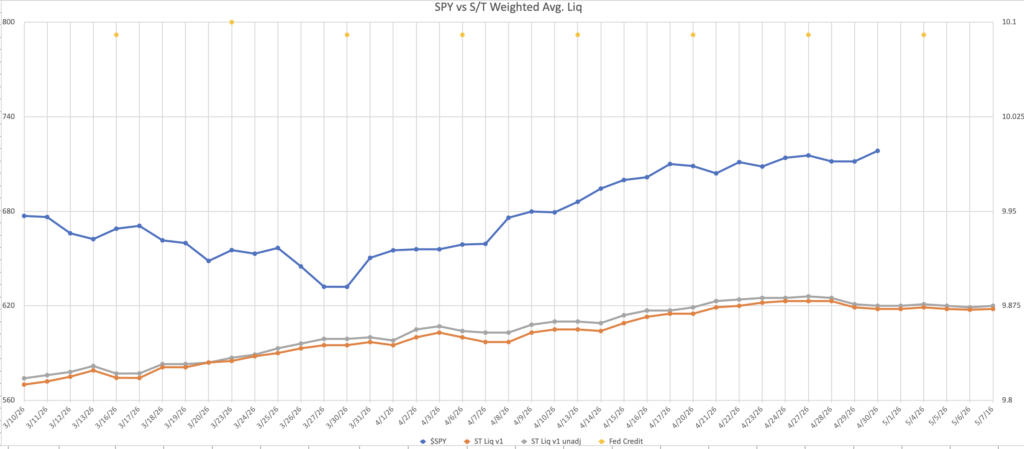

As of 04/30 NY Market close, liquidity stays very flat into 05/07. The market continues to hit new highs despite some mixed reactions to tech earnings.

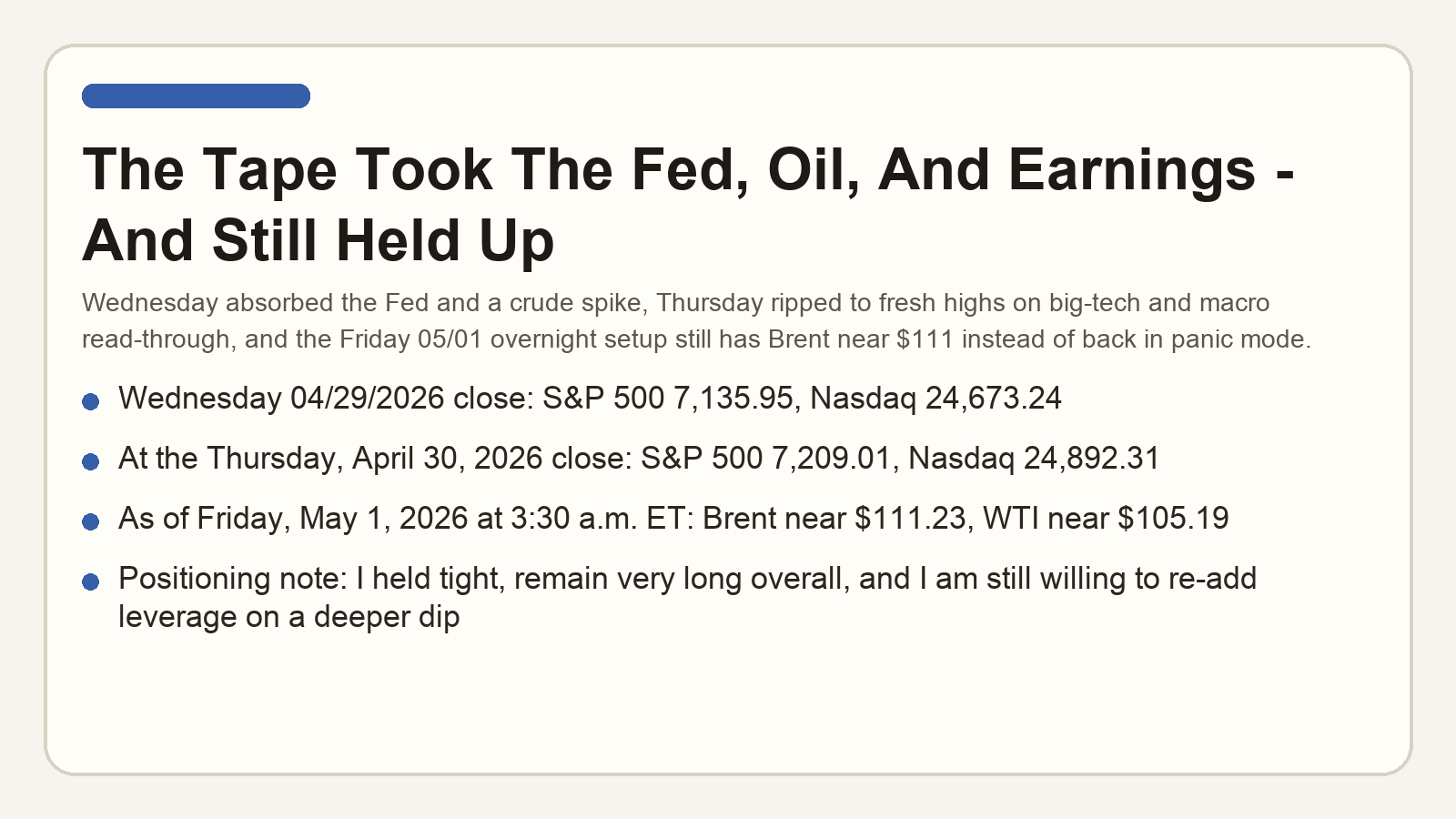

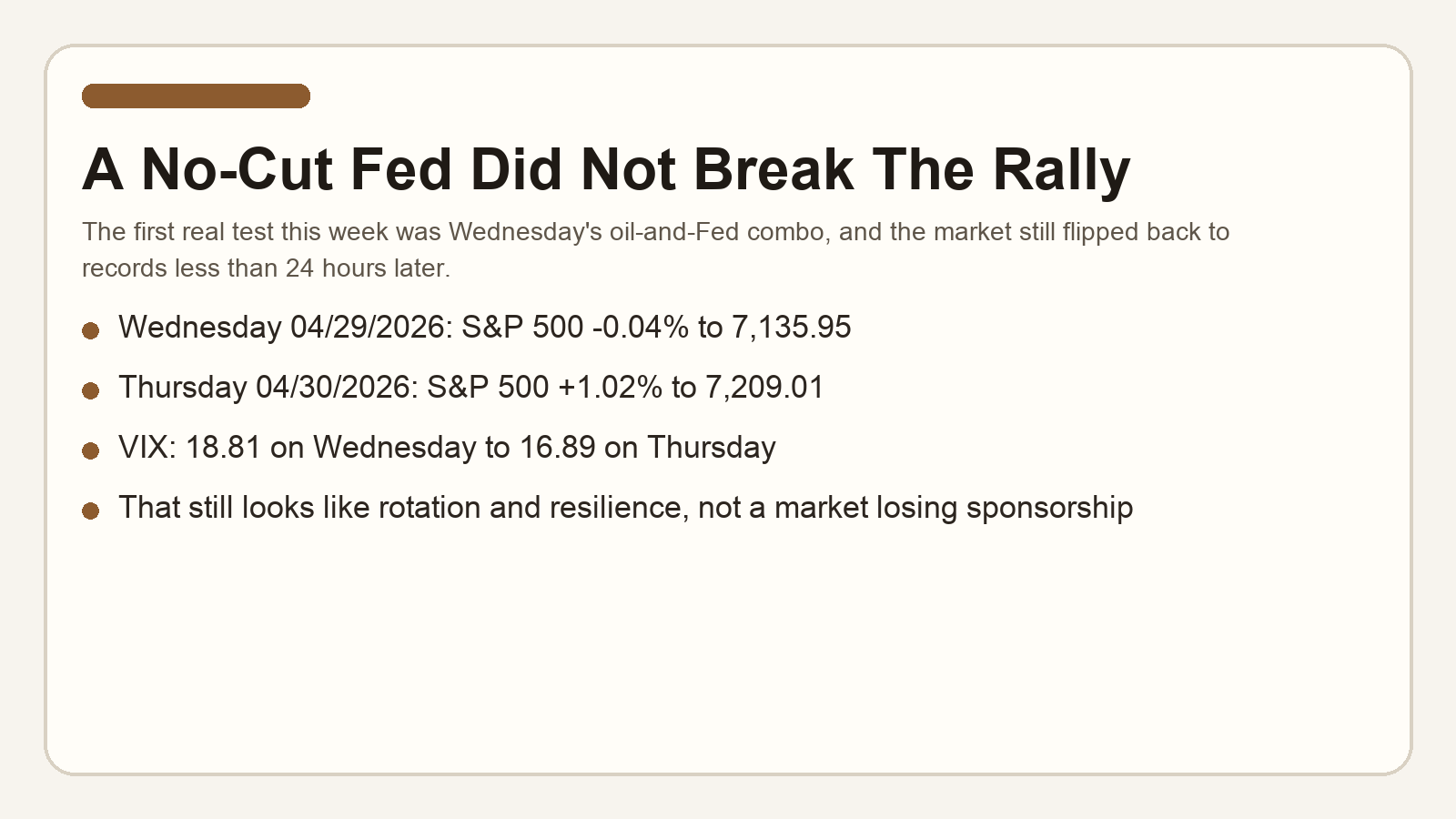

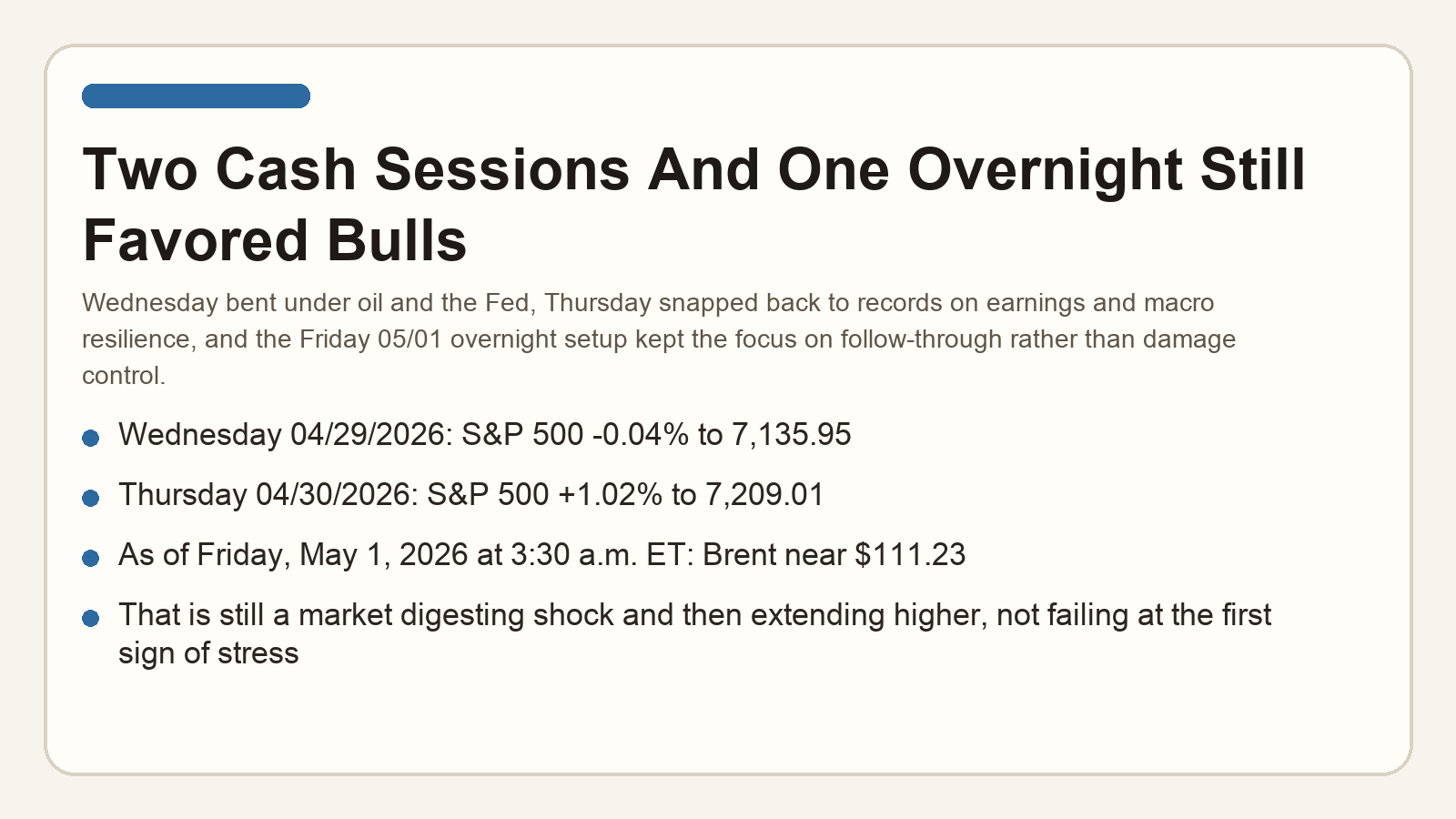

Since the last roadmap, the market has still not broken character. Wednesday 04/29/2026 absorbed a no-cut Fed, a crude spike, and a mixed first wave of megacap earnings without truly breaking down, but it is also true that Microsoft and Meta both dropped hard after reporting even though the underlying businesses still looked strong. Thursday 04/30/2026 then turned right back around, with the S&P 500 and Nasdaq closing at fresh highs as growth data held up, claims stayed low, and the market rewarded enough of the big-tech setup to keep the broader tape constructive. Then As of Friday morning, the focus was still on whether Apple, Amazon, Microsoft, Meta, and Alphabet had done enough to keep the AI and consumer story alive while Brent held near $111.23. I trimmed a significant amount of Google as it ripped to new highs and used that cash to buy more MSFL, METU, META, and MSFT. I remain very long overall and I am still willing to re-add more leverage on a deeper dip.

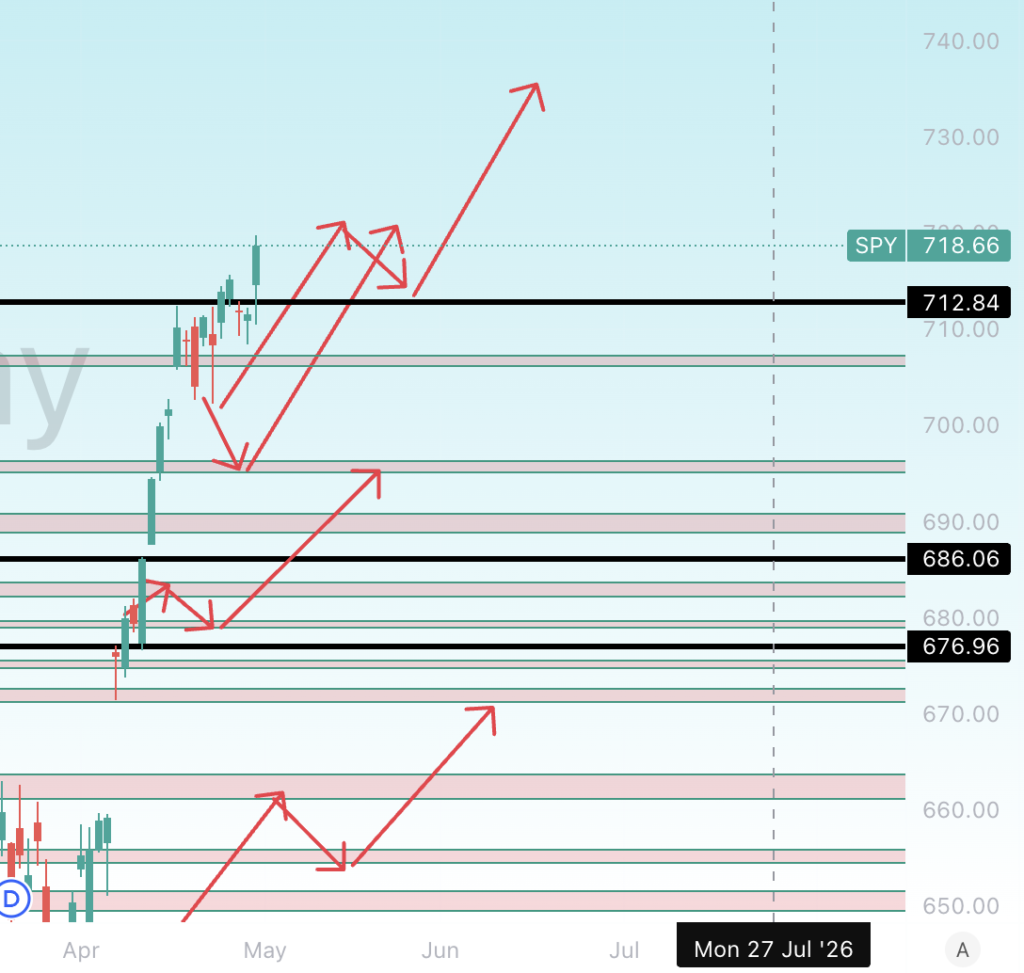

At the Thursday, April 30, 2026 close, SPY finished at $718.66 versus Wednesday’s $711.58 close, a +0.99% move. That is not what a market on the verge of failure looks like after taking a Fed hold, hotter PCE, and an oil scare all inside two sessions.

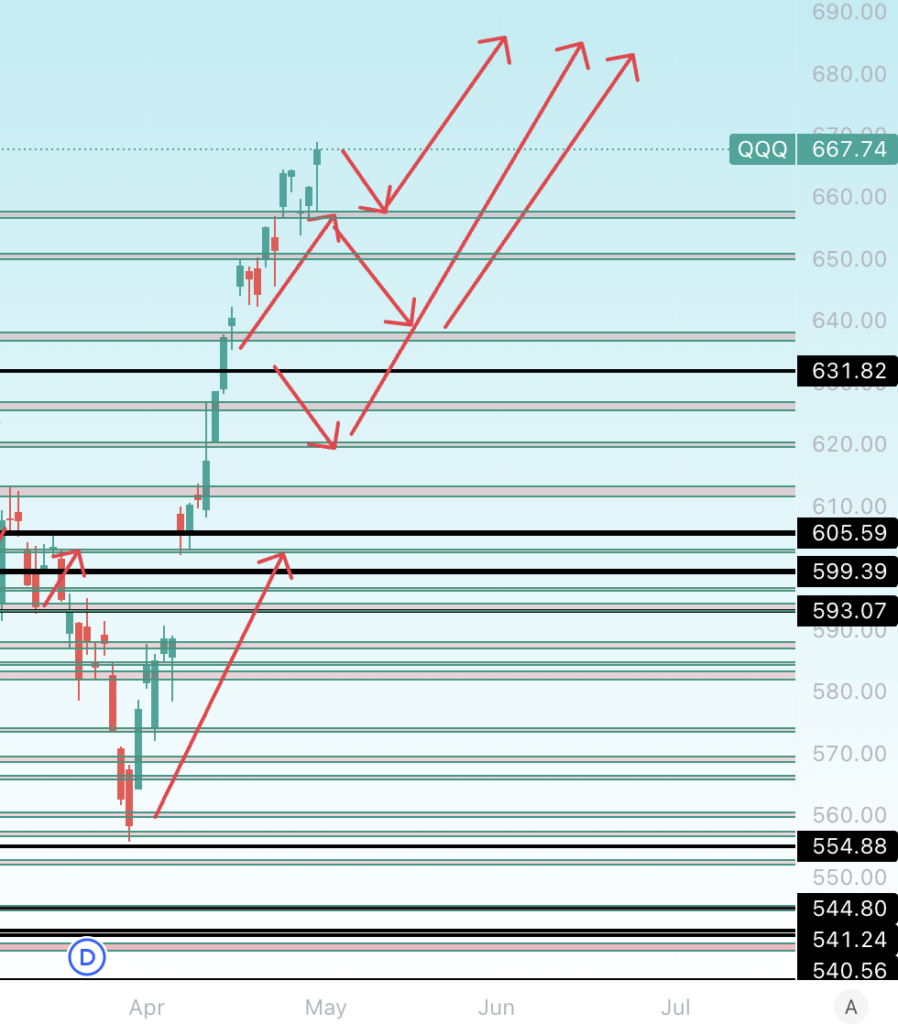

Tech leadership also did not disappear. At the Thursday, April 30, 2026 close, QQQ finished at $667.74 versus Wednesday’s $661.57 close, up +0.93%, while XLK closed at $159.50 versus $159.11, up +0.25%. That still looks like the right part of the tape doing the lifting even though megacap tech performance was divided.

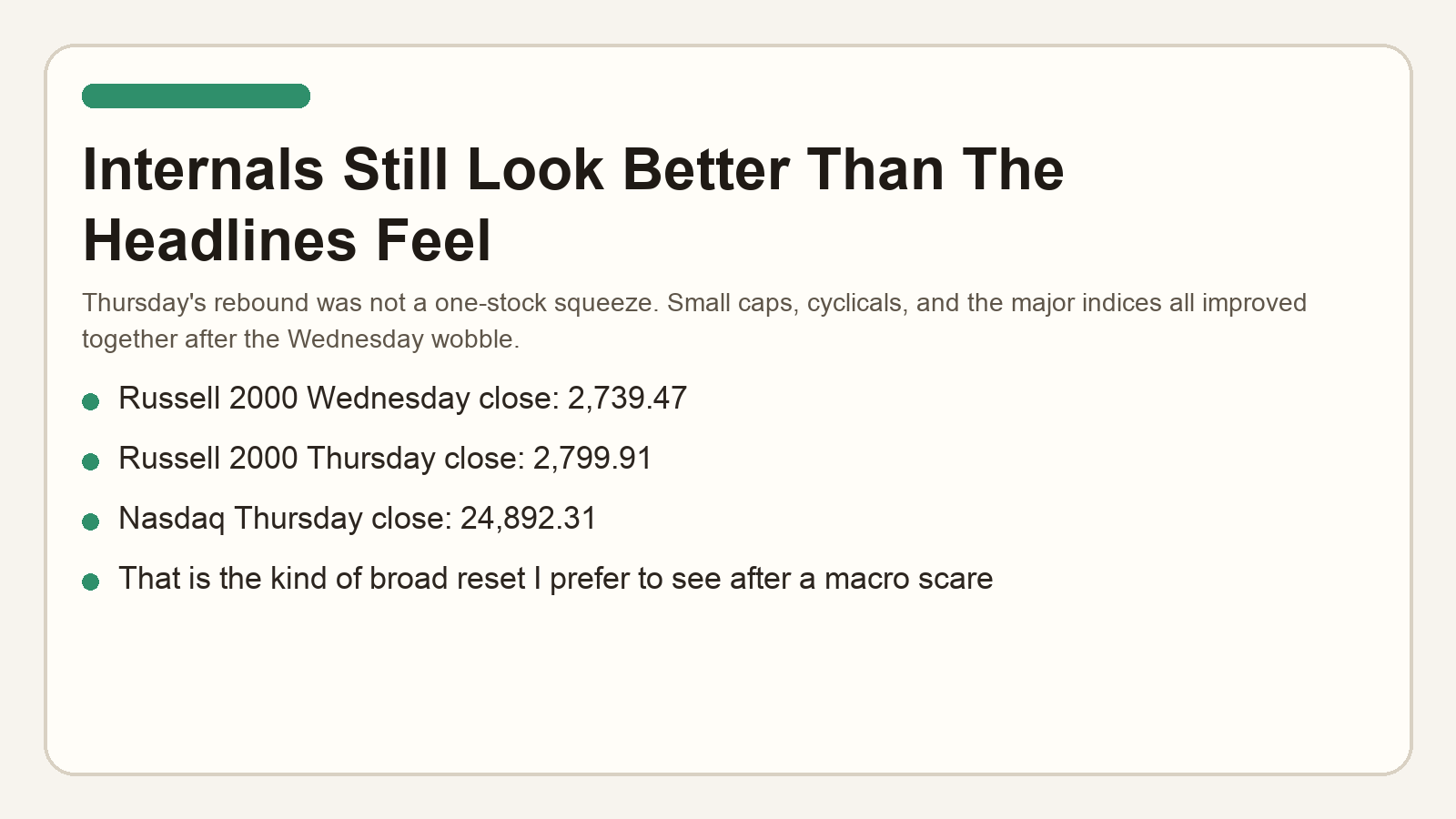

The internal tone still looks constructive to me. Wednesday 04/29/2026 was the session that should have done real damage if bulls were wrong: oil jumped, the Fed did not ease, and the first after-hours reactions in big tech were mixed. Instead, Thursday 04/30/2026 turned into a broad reclaim. When a market can take that kind of test and still print records 24 hours later, it’s a bullish sign.

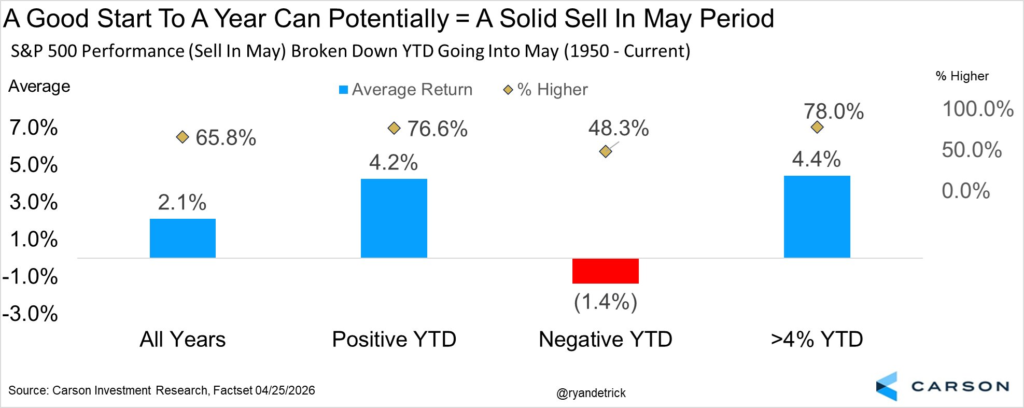

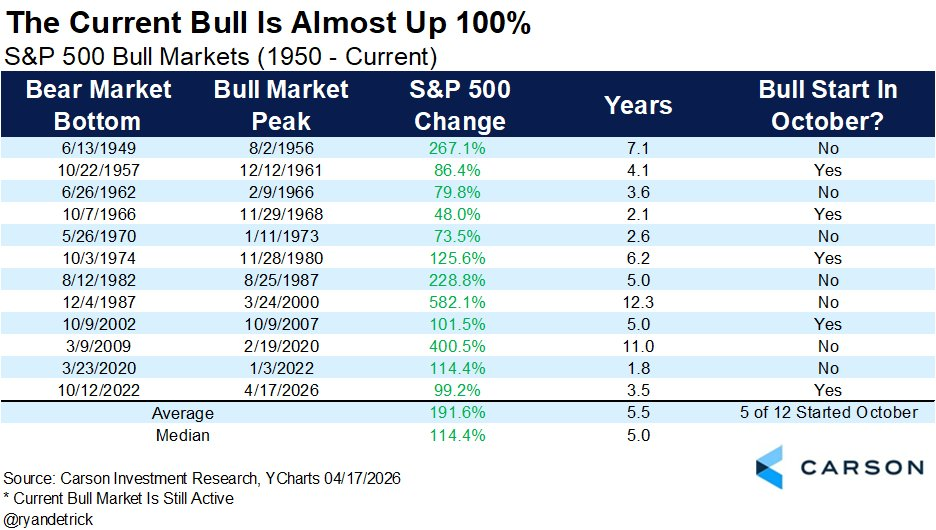

Credit: @RyanDetrick. The bigger point from the seasonality work is still that strong thrusts into May tend to overpower the old sell-in-May cliché more often than people remember. When momentum is already in the tape, I would rather respect it than fight it.

Seasonality, breadth, and the internals all improved

Breadth still looked better than the skepticism did. The Russell 2000 closed Wednesday 04/29/2026 at 2,739.47 and then Thursday 04/30/2026 at 2,799.91, a +2.21% move. That is exactly the kind of participation I want to see if the market is going to keep pressing higher from here.

The thrust backdrop still looks bullish. Wednesday’s pullback only took the S&P 500 down 0.04% even with Brent settling at $112.63, and Thursday then pushed the index right back to 7,209.01. That is a pause inside momentum, not momentum failing.

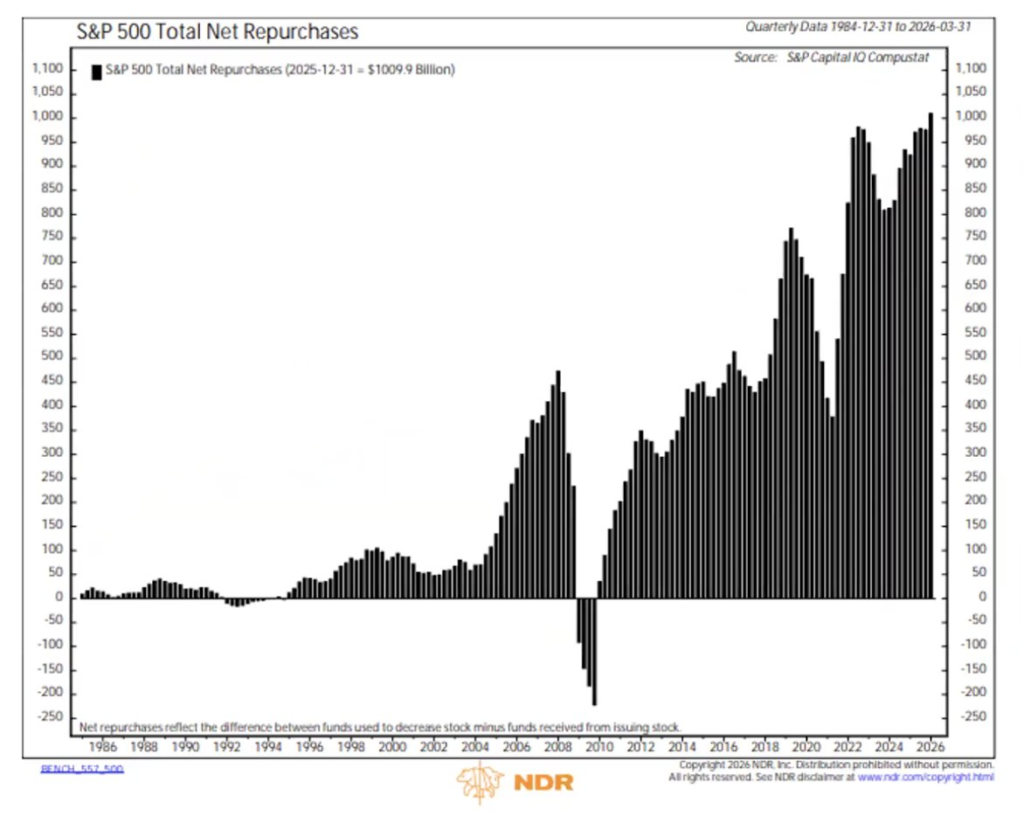

Corporate buybacks are another reason I still do not want to overreact to every scary headline. The underlying support under the index remains real, and that matters even more when traders are trying to decide whether higher oil or tighter policy should matter more than earnings and cash flows.

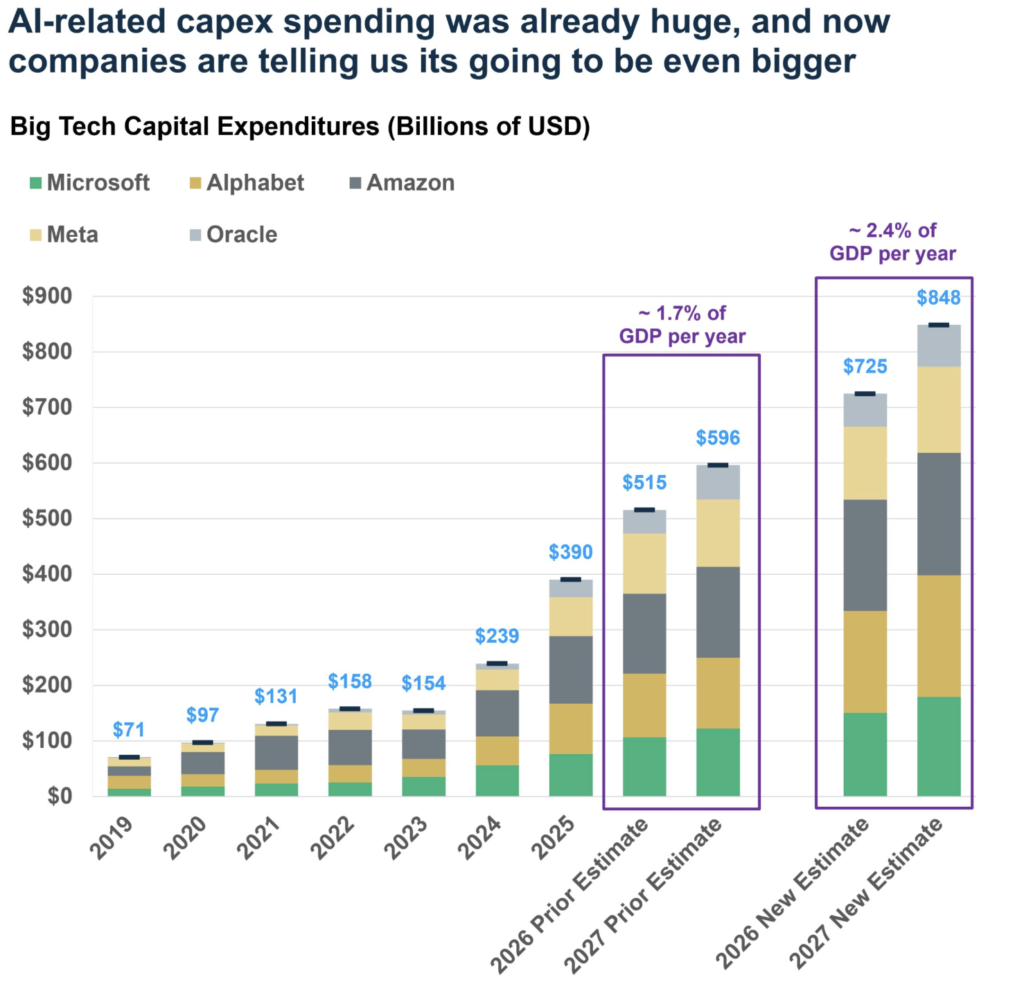

Big tech continues to invest more and more into AI and rightfully so. These companies will profit the most and remain the leaders due to this heavy spend.

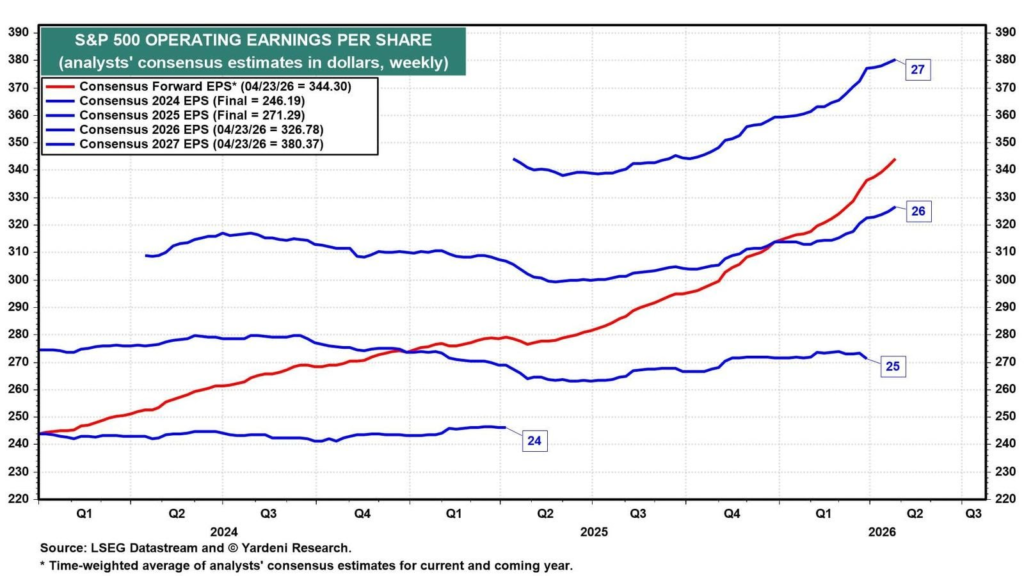

Forward earnings are still one of the better bull arguments on the board. If the market were genuinely rolling into a deeper problem, I would expect forward S&P 500 EPS and the quality of the earnings tape to be deteriorating together. Instead, what we are really seeing is a market forcing the biggest AI spenders to justify the spend while the broader earnings base still mostly behaves.

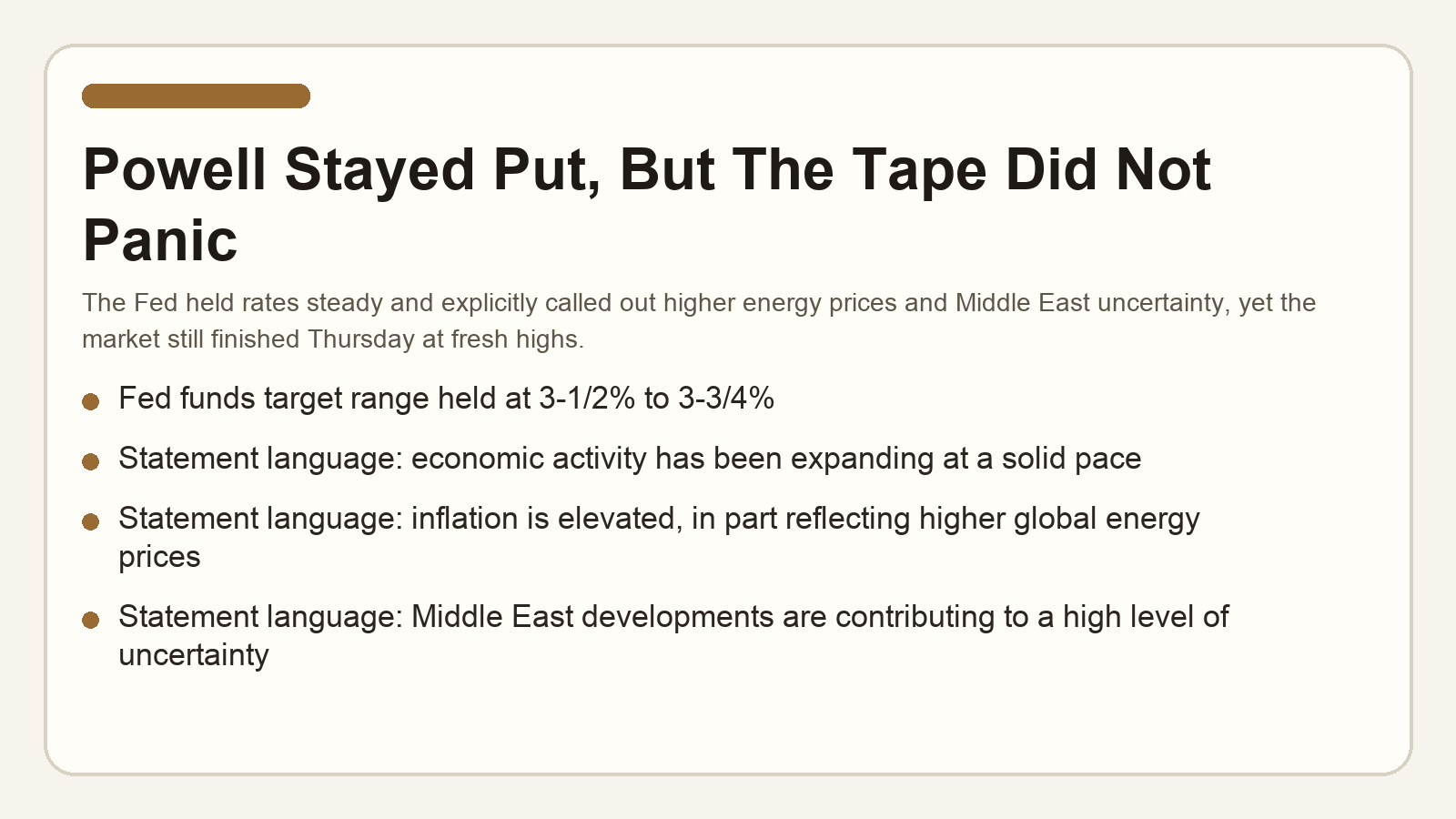

The Fed gave us a cleaner line in the sand on Wednesday 04/29/2026. The Committee held the target range at 3-1/2% to 3-3/4% and said economic activity has been expanding at a solid pace, while also noting that inflation is elevated in part because of higher global energy prices and that Middle East developments are adding uncertainty. That was not dovish, but the tape still got over it quickly.

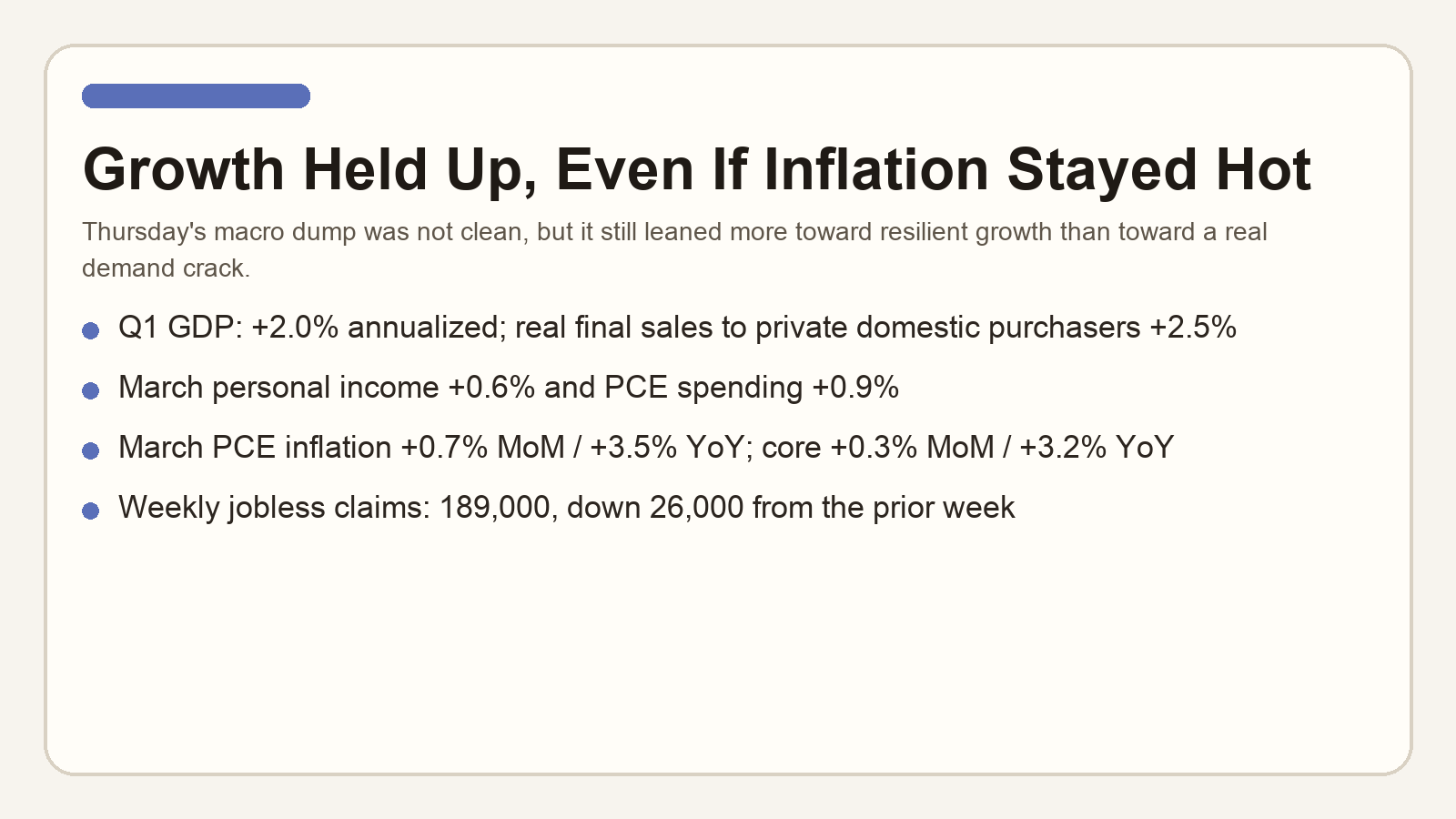

Thursday 04/30/2026 macro then looked more like resilient growth with sticky inflation than like a demand collapse. Q1 GDP came in at +2.0% annualized, real final sales to private domestic purchasers still rose +2.5%, March personal income increased +0.6%, spending rose +0.9%, and initial jobless claims fell to 189,000. The inflation side stayed hot, with headline PCE +0.7% month over month and +3.5% year over year, but the market still chose to lean into growth and earnings.

The bigger bull-market backdrop still matters too. We are well into a mature uptrend that has already survived war headlines, hot inflation prints, and multiple capex scares. That does not mean every dip is a buy with no thought. It does mean I do not want to confuse a volatile rotation with a true break in character.

Market recap: Wednesday 04/29 through Thursday 04/30, plus the Friday 05/01 overnight setup

Wednesday 04/29/2026: S&P 500 -0.04% to 7,135.95. Dow -0.57% to 48,861.81. Nasdaq +0.04% to 24,673.24. Oil and the Fed were the main drivers in cash trading, while Microsoft and Meta then drove the after-hours debate by printing strong quarters but also re-centering the market on AI-spend intensity.

Thursday 04/30/2026: S&P 500 +1.02% to 7,209.01. Dow +1.62% to 49,652.14. Nasdaq +0.89% to 24,892.31. The macro dump did not look soft enough to force a rate-cut celebration, but it was strong enough to keep growth fears muted, and Alphabet plus Amazon helped keep the megacap earnings backdrop constructive.

Thursday night 04/30/2026 into As of Friday, May 1, 2026 at 3:30 a.m. ET: Apple reported its best March quarter ever with revenue of $111.2 billion and diluted EPS of $2.01, U.S. futures edged higher, and Brent held near $111.23 rather than launching into another panic squeeze. That overnight tone matters because it says the market was still focused on confirmation, not on damage control.

That whole sequence is why I am still leaning bullish. Wednesday was the session that gave bears their best opening. Thursday answered with records. The overnight setup into Friday still had oil elevated but not spiraling and big-tech earnings still largely reinforcing that AI spending is real, monetization is real, and the consumer has not fallen apart. That is still a constructive combination.

Oil and volatility are still important, but not in control

Oil clearly still matters, but it is no longer dictating every single tick. Wednesday 04/29/2026 Brent settled at $112.63 and hit the tape alongside the Fed. Thursday 04/30/2026 Brent then settled back at $110.40 even while equities pushed to records. That is a huge difference from the late-March panic phase.

Volatility also backed off fast once the market decided the growth and earnings story still outranked the energy scare. At the Thursday, April 30, 2026 close, VIX finished at 16.89 versus Wednesday’s 18.81 close. Then As of Friday, May 1, 2026 at 3:30 a.m. ET, Brent was only around $111.23. That still looks like a market that can absorb oil risk rather than one trapped by it.

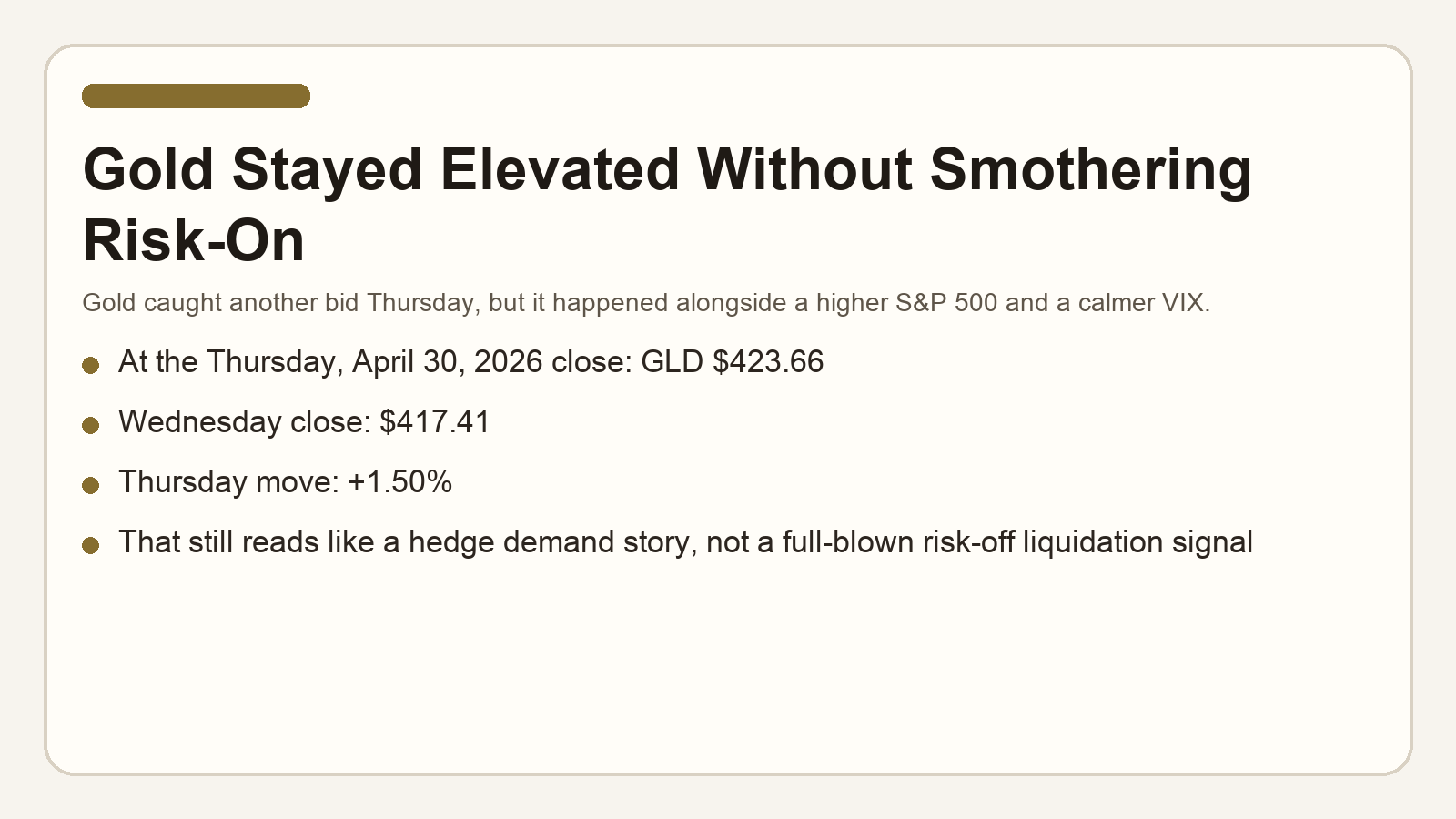

Gold is elevated, but not blocking risk appetite

Gold is still elevated, but it is not stopping risk-on behavior. At the Thursday, April 30, 2026 close, GLD finished at $423.66 versus Wednesday’s $417.41 close, up +1.50%. I still like the hedge case in gold, but Thursday showed it can coexist with a higher S&P 500 just fine.

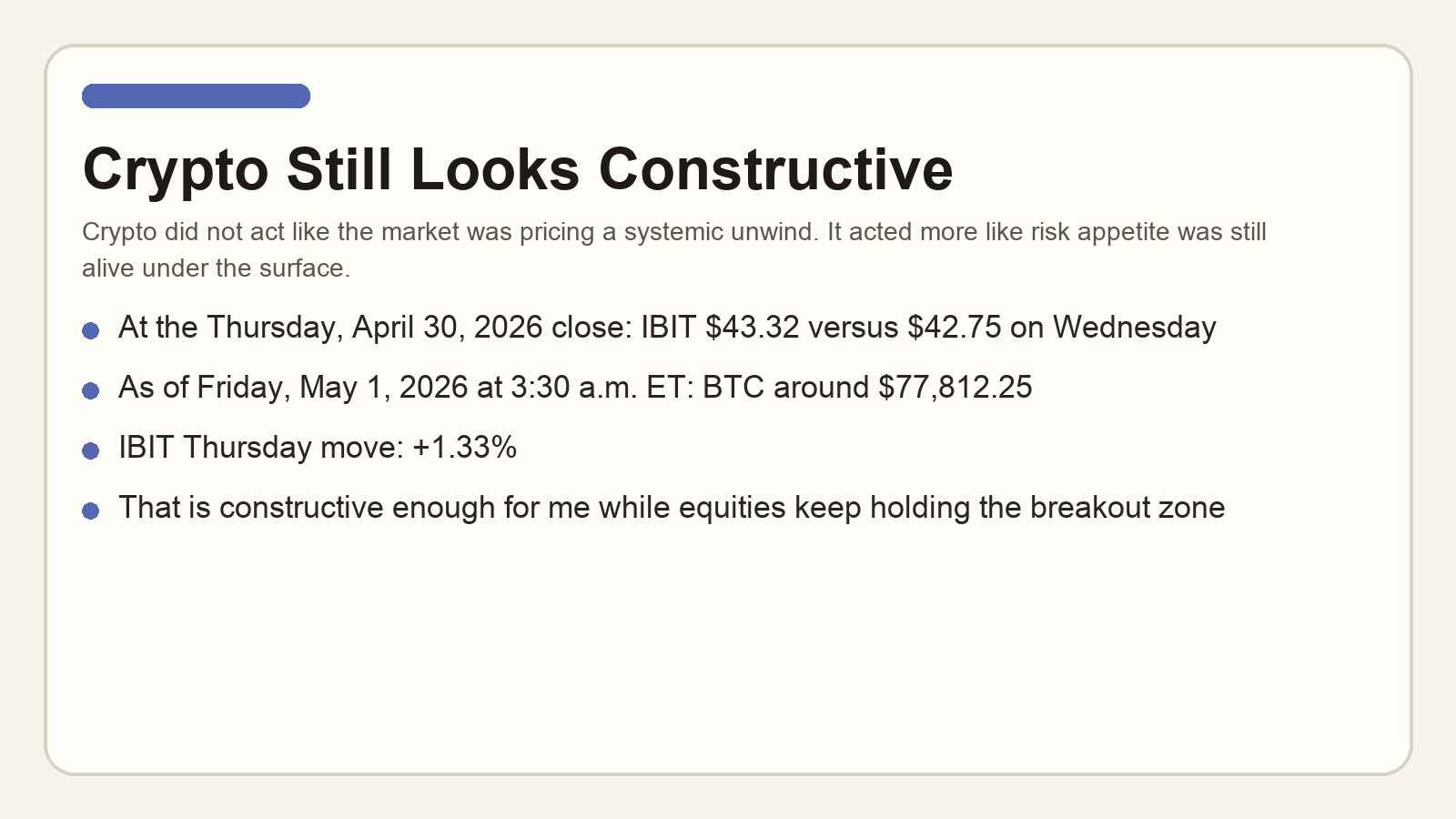

Crypto remains constructive

Crypto also still reads more constructive than threatening. At the Thursday, April 30, 2026 close, IBIT closed at $43.32 versus $42.75 on Wednesday, up +1.33%. BTC is around $78K and I think consolidating for a big breakout. I remain long crypto.

Amazon continues acting like a leader

Amazon still looks like one of the cleaner leadership names in the tape. At the Thursday, April 30, 2026 close, AMZN finished at $265.06 versus Wednesday’s $263.04 close, up +0.77%. That is exactly the kind of post-report behavior I want if institutions are still rewarding quality growth.

I also still lean bullish on the business reaction, not just the chart. Amazon reported Q1 net sales of $181.5 billion, up 17%, AWS sales of $37.6 billion, up 28%, and operating income of $23.9 billion. The Q2 guide for net sales of $194.0 billion to $199.0 billion and operating income of $20.0 billion to $24.0 billion still looks supportive. AWS growth, retail efficiency, and ad leverage all still point the right way. I remain long via $AMZU although my sold covered calls should reduce my exposure.

META remains a big opportunity

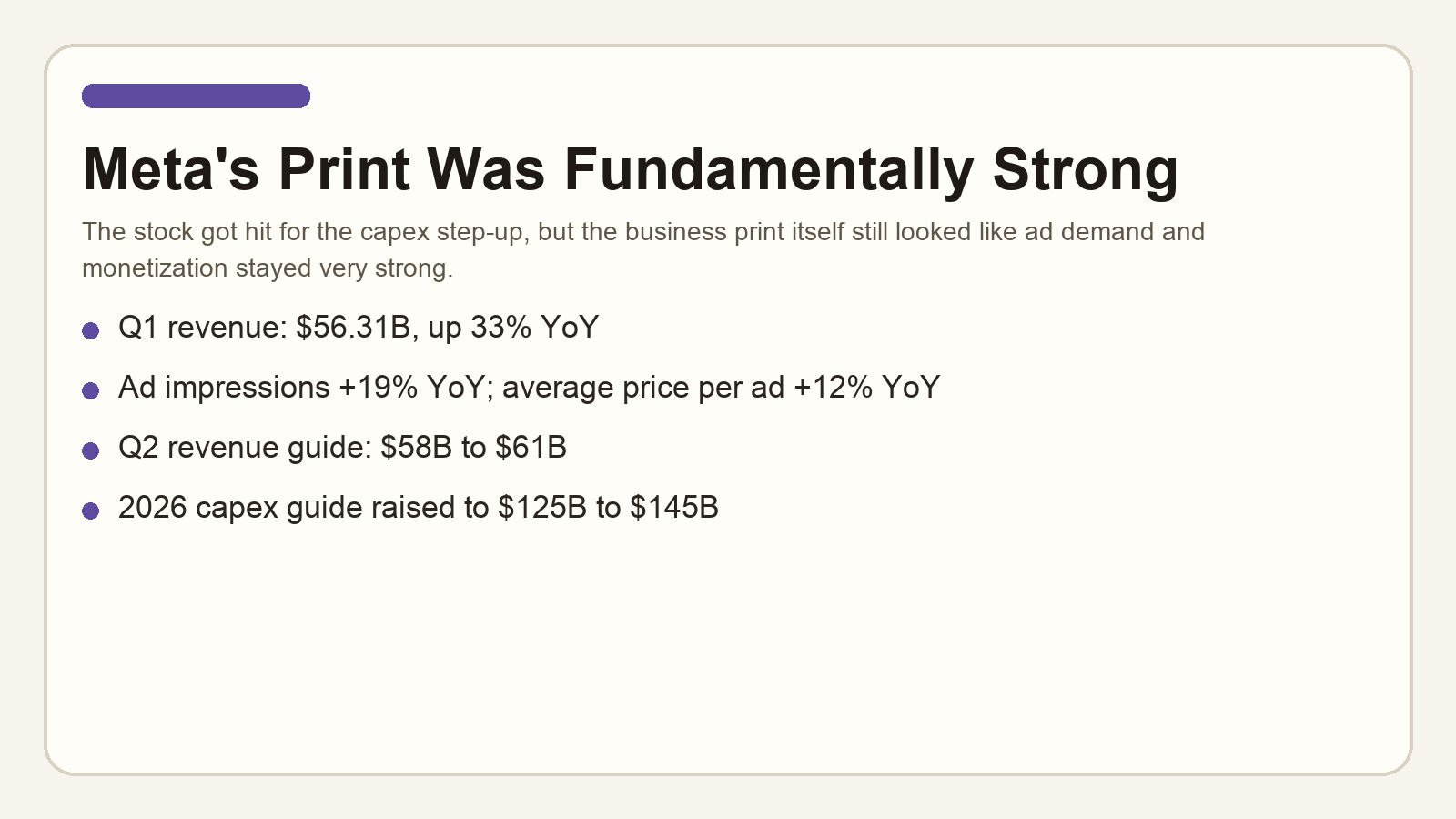

META took the hardest obvious post-earnings hit in this group. At the Thursday, April 30, 2026 close, META finished at $611.91 versus Wednesday’s $669.12 close, down 8.55%. That is a real drawdown, but I still think it looks more like a capex repricing than a thesis break.

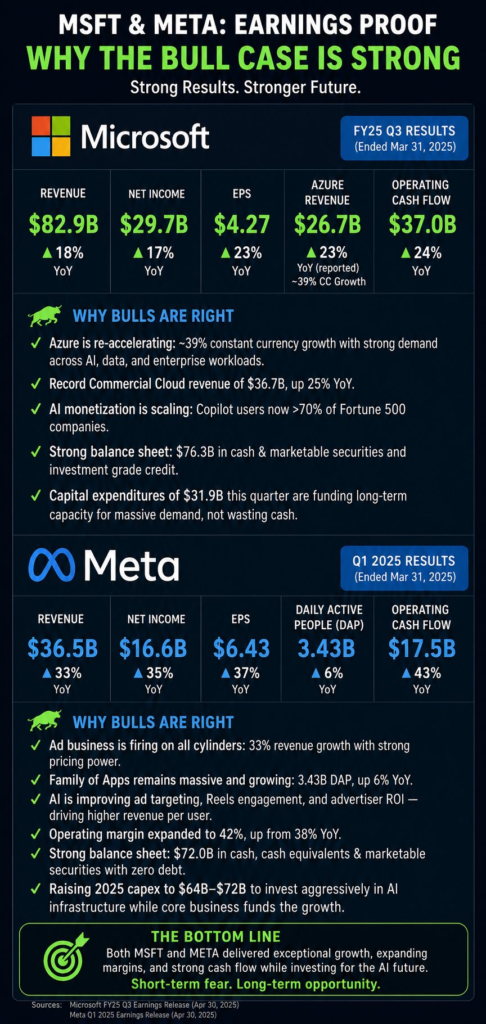

The underlying quarter was still very strong. Meta reported Q1 revenue of $56.31 billion, up 33% year over year, with ad impressions up 19% and average price per ad up 12%. The company then guided Q2 revenue to $58 billion to $61 billion. The stock got hit because capex is now expected at $125 billion to $145 billion for 2026, but to me that still looks like investment into strength rather than evidence that monetization is failing.

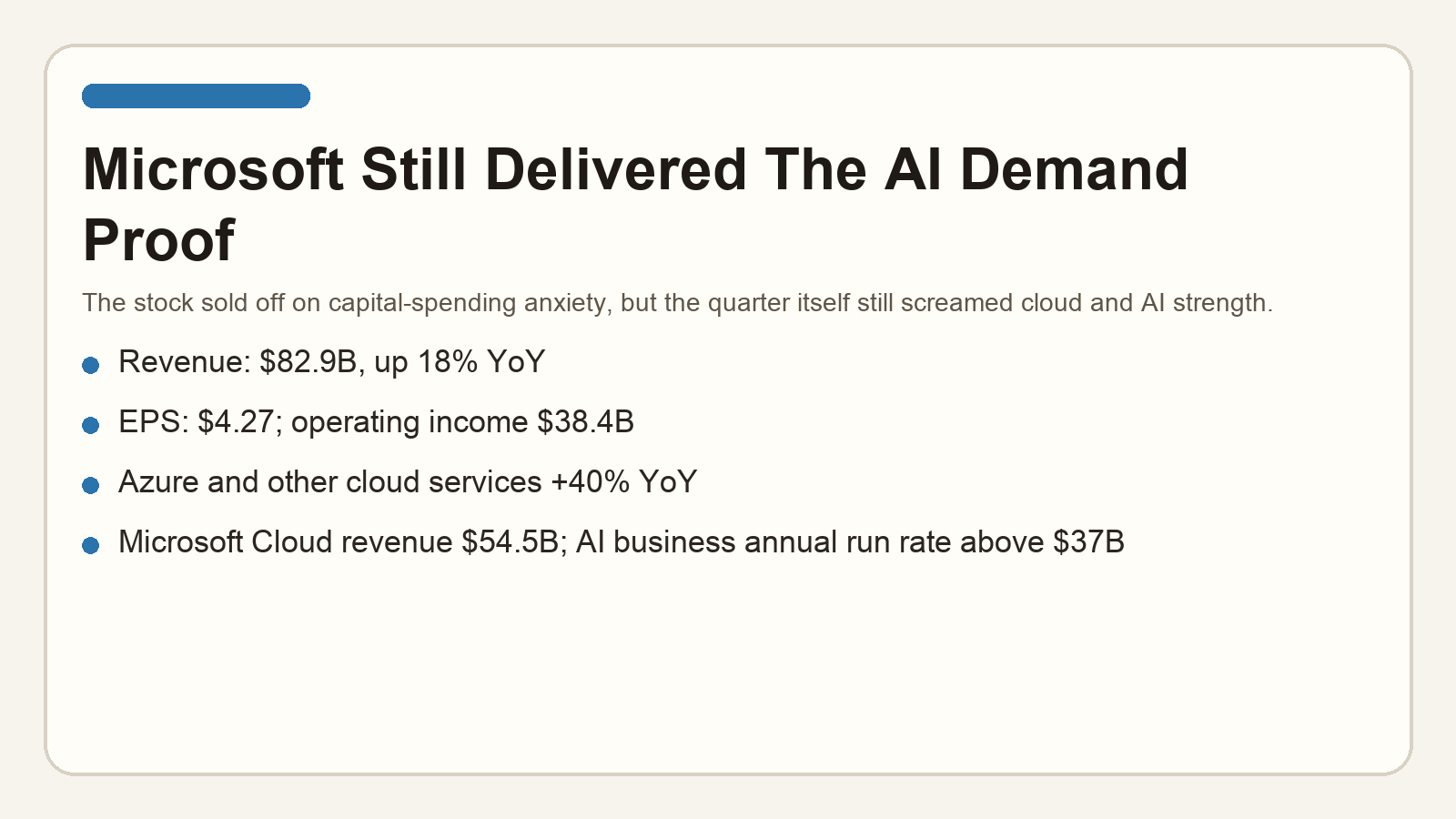

MSFT – a steal

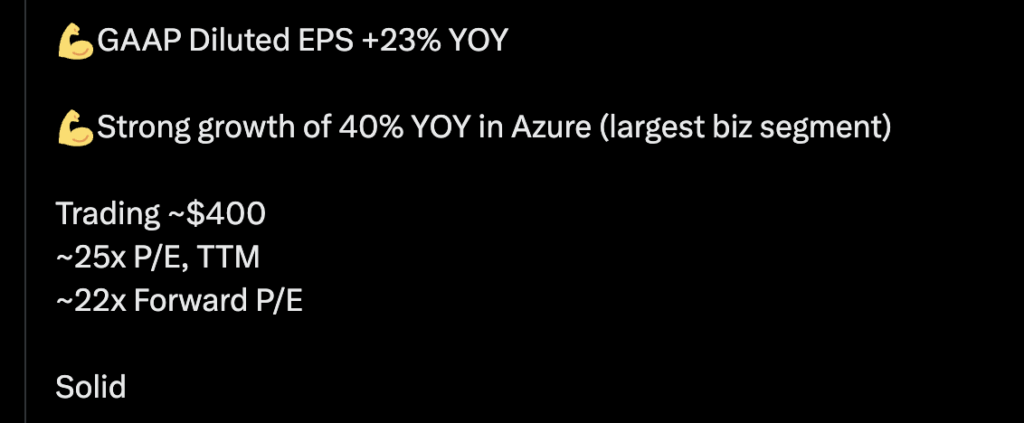

Microsoft did not escape the capital-spending debate either. At the Thursday, April 30, 2026 close, MSFT finished at $407.78 versus Wednesday’s $424.46 close, down 3.93%. But I still do not think the price action invalidates what the quarter said.

The quarter itself looked bullish. Microsoft reported revenue of $82.9 billion, up 18%, operating income of $38.4 billion, and EPS of $4.27. Azure and other cloud services grew 40%, Microsoft Cloud revenue reached $54.5 billion, and management said the AI business annual revenue run rate has already topped $37 billion. If the stock needs a beat-and-absorb phase because investors are nervous about capex, that is still very different from the business rolling over.

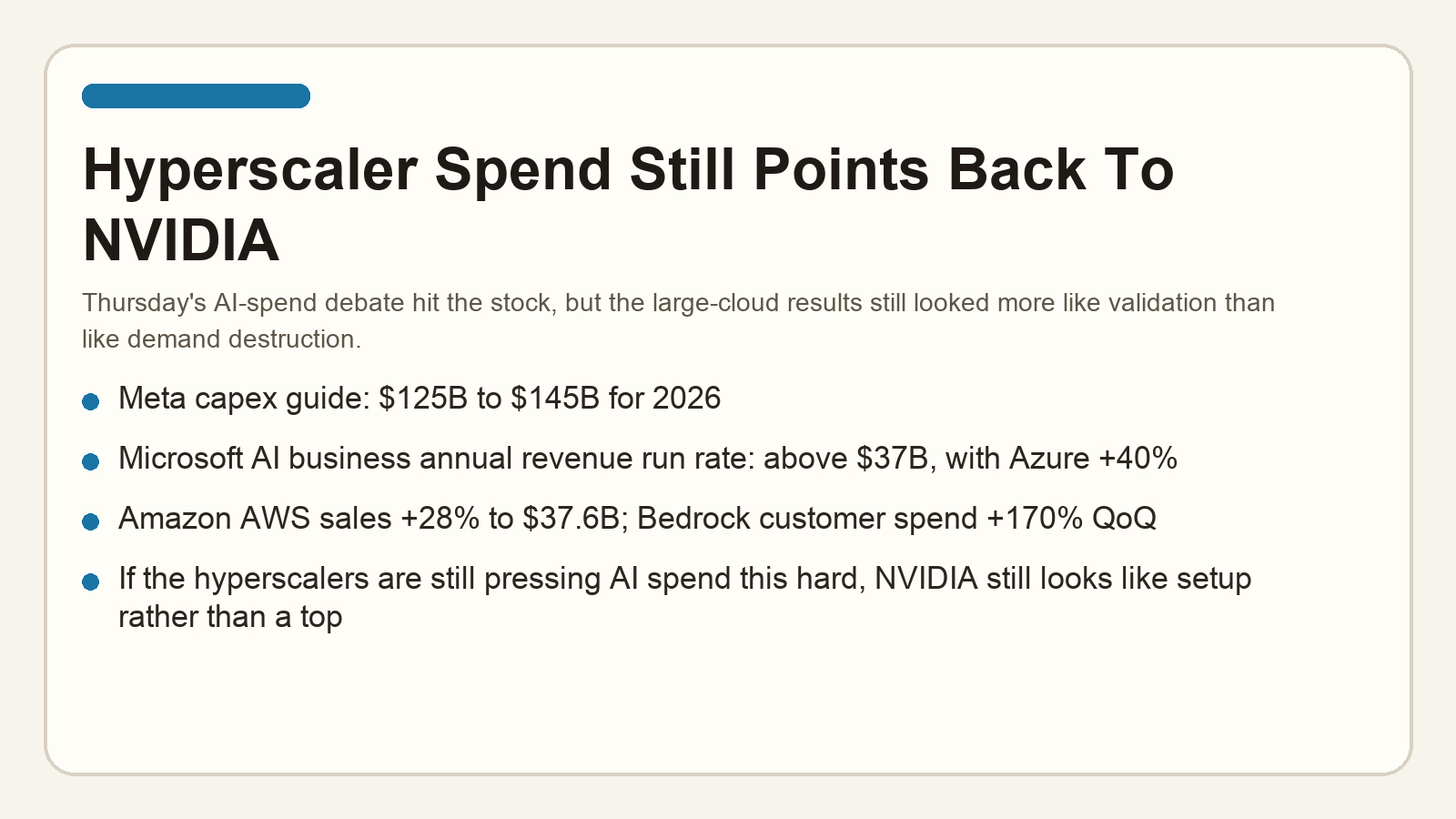

NVDA remains the first stop for AI beta

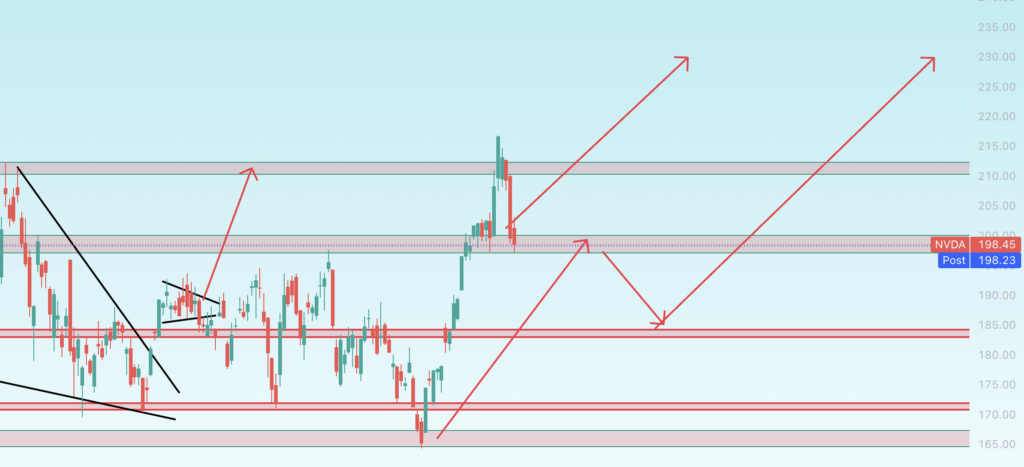

NVDA is still the cleanest AI beta read-through in the group. At the Thursday, April 30, 2026 close, NVDA finished at $199.57 versus Wednesday’s $209.25 close, down 4.63%. That was not pleasant, but it came inside a session where investors were actively questioning how much AI spend is too much.

I still lean bullish on that setup. Microsoft just showed Azure growth of 40% and an AI revenue run rate above $37 billion. Meta just raised its 2026 capex range to $125 billion to $145 billion. Amazon just grew AWS 28% to $37.6 billion and said Bedrock customer spend grew 170% quarter over quarter while the chips business topped a $20 billion annual revenue run rate. Alphabet also helped lead Thursday’s rally after its own strong print. That still looks like later-May support for NVIDIA more than the start of an AI unwind. It has been in the same range for far too long and is undervalued iMO.

Key catalysts from here

From here I care about four things most. First, whether Friday’s cash session confirms that Thursday’s record close can survive the full post-earnings digestion from Apple, Amazon, Meta, Microsoft, and Alphabet. Second, whether Brent can stay near the low-$110s instead of ripping right back toward the panic highs. Third, whether next week’s trade data and JOLTS keep the resilient-demand story intact. Fourth, whether the market can take one more turn through jobs and inflation without losing the April breakout zone. If those pieces keep landing cleanly, I still think the higher-probability move is up.

Upcoming key events and dates

- 05/05/2026 – U.S. International Trade in Goods and Services for March 2026, 8:30 a.m. ET

- 05/05/2026 – Job Openings and Labor Turnover Survey for March 2026, 10:00 a.m. ET

- 05/05/2026 – New Residential Sales for March 2026, 10:00 a.m. ET

- 05/07/2026 – Productivity and Costs for Q1 2026, 8:30 a.m. ET

- 05/08/2026 – Employment Situation for April 2026, 8:30 a.m. ET

- 05/12/2026 – Consumer Price Index for April 2026, 8:30 a.m. ET

- 05/13/2026 – Producer Price Index for April 2026, 8:30 a.m. ET

- 05/14/2026 – U.S. Import and Export Price Indexes for April 2026, 8:30 a.m. ET

- 05/14/2026 – Advance Monthly Sales for Retail and Food Services for April 2026, 8:30 a.m. ET

Bottom line: Wednesday 04/29/2026 and Thursday 04/30/2026 were exactly the kind of back-to-back tests that can expose a weak rally. Instead, the market absorbed a no-cut Fed, higher oil, hotter inflation, and a fresh round of AI capex angst, then still closed Thursday at record highs. As of Friday, May 1, 2026 at 3:30 a.m. ET, the setup was still about follow-through, not failure. I have re-added more leverage to the beaten down mega cap stocks, remain very long overall, and I am still willing to re-add more leverage on a deeper dip.

Disclaimer: The information provided in this post is for educational and informational purposes only and does not constitute financial advice, investment advice, trading advice, or any other form of professional advice. The author is not a registered investment advisor, broker-dealer, or financial planner. No content published here should be interpreted as a recommendation to buy, sell, or hold any security or financial instrument.

All investments and trading strategies involve risk, including the possible loss of principal. Past performance is not indicative of future results. You should conduct your own research and consult with a licensed financial professional before making any investment decisions. The author expressly disclaims any liability for any loss or damage arising from reliance on the information contained herein.